A microeconomic analysis of the Colombian tax on ultra-processed food (Ley 2277)

Giuliano Bianchi*

EHL Hospitality Business School, HES-SO, University of Applied Sciences and Arts Western Switzerland (Suiza)

Recibido: 22 de abril del 2025 | Aceptado: 14 de agosto del 2025

Cómo citar: Bianchi, Giuliano. “A microeconomic analysis of the Colombian tax on ultra-processed food (Ley 2277)”. Latin American Law Review n.º 15 (2025): 1-15, doi https://doi.org/10.29263/lar15.2025.01

Abstract

This article presents a microeconomic analysis of Colombia’s “healthy tax” on ultra-processed foods introduced by Law 2277. Its hybrid design —based on both ultra-processing and nutrient thresholds— is framed as a Pigouvian response to negative externalities. Tax-incidence analysis suggests that, although the tax is legally levied on producers, much of the burden is passed on to consumers, as inelastic demand limits effects on quantities while raising consumer costs. Substitution and income effects are also considered, with preliminary evidence pointing to greater impacts on low-income households due to differences in demand elasticities. Available data suggest modest reductions in consumption, yet consumers need time to adjust their behavior and health outcomes emerge only with delay. Because health is a lagging indicator, economic analysis must be complemented with epidemiological research, to determine whether observed changes lead to meaningful improvements in public health.

Keywords

Ultra-processed foods, Health taxes, Tax incidence, Law and economics, Distributional effects, Public health outcomes.

Un análisis microeconómico del impuesto colombiano a los alimentos ultraprocesados (Ley 2277)

Resumen

Este artículo presenta un análisis microeconómico del “impuesto saludable” colombiano a los alimentos ultraprocesados introducido por la Ley 2277. Su diseño híbrido—basado en la condición de ultraprocesado y en umbrales nutricionales—se interpreta como una respuesta pigouviana a externalidades negativas. El análisis de incidencia tributaria sugiere que, aunque el impuesto recae legalmente sobre los productores, gran parte de la carga se traslada a los consumidores, ya que una demanda inelástica limita los efectos sobre las cantidades pero aumenta los costos para estos. También se consideran los efectos de sustitución y de renta, y la evidencia preliminar apunta a mayores impactos en hogares de bajos ingresos debido a diferencias en elasticidades de la demanda. Los datos disponibles sugieren reducciones modestas en el consumo, aunque los consumidores requieren tiempo para ajustar su comportamiento y los efectos en salud se manifiestan con retraso. Dado que la salud es un indicador rezagado, el análisis económico debe complementarse con estudios epidemiológicos que evalúen si los cambios observados generan mejoras significativas en salud pública.

Palabras clave

Alimentos ultraprocesados, Impuestos saludables, Incidencia tributaria, Análisis económico del derecho, Efectos distributivos, Resultados en salud pública

___________________________________________________________________________

Introduction

This study conducts a microeconomic1 analysis of the newly introduced tax on “junk food” in Colombia (Ley 2277). Colombia was the first country in the Americas to introduce a “junk food” law targeting processed food2. The idea behind this tax is to discourage the consumption of ultra-processed food3.

Junk food is loaded with trans fats, which can lead to health problems such as diabetes, obesity and menstruation issues4, just to name a few. It is also linked to mental health issues such as anxiety and depression5.

The tax aims to address urgent public health issues in Colombia where 56.4% of the population is overweight, 40% suffers from cardiovascular problems, and 76% die of non-communicable diseases6. The culprit is another public health nightmare: sodium. With a daily intake of 12g per person, Colombians are the biggest consumers of salt in Latin America7.

Public intervention is justified, according to some scholars, as the economic forces of the free market push consumers towards unhealthy lifestyles, and the only safety net is the legislative action of the government8. According to some scholars, one of the problems that policymakers face is the junk food lobby9. The Colombian legislator overcame such obstacles and, in 2022, a new law went into effect.

The new law (Ley 2277 of 2022) in force as of 1 November 2023 modified the tax law and introduced two new taxes on “sugar-sweetened ultra-processed” beverages and on ultra-processed food products10. The tax is being phased in: for 2023 the tax was 10%, in 2024 it was set at 15%, and in 2025 it was raised to 20%11.

More formally, art. 513-1 of the Colombian tax law defines which beverages should be considered ultra-processed, while art. 513-6 defines what should be considered ultra-processed food12. Finally, Art. 513-1 defines who sustains the tax (i.e., producers, sellers, and importers)13. Intuitively, ultra-processed food is food that contains ingredients that are not commonly found in a household kitchen14.

The policymakers who levied the tax believe that producers or retailers will pass the tax onto consumers, which will eventually reduce the consumption of unhealthy products. Ideally, the tax will target the low-income population, which is the segment that i) consumes the most junk food and ii) is the most cost-conscious and thus responsive to a tax15.

Nonetheless, a microeconomic analysis may provide other insights. Firstly, microeconomic analysis allows us to put the tax in context. The tax is being used to address a situation defined by economic theory as a “negative externality”. In the presence of externalities, the market fails to be efficient, so public intervention is justified16.

Secondly, the price elasticity analysis could shed light on who would, eventually, bear the tax (the consumer or the producers/seller) and to what extent. Likewise, income elasticity provides insight into which type of population is actually financially affected: the lower or higher income class. Furthermore, the Slutsky/Hicksian decomposition would help us understand how consumers will adjust their consumption habits (if at all) and how this tax affects their consumption basket.

The study is organized as follows. The first part of the study will present the legal framework. In particular, the study aims to establish a framework encompassing the new law’s historical and teleological aspects. The second part of the project aims to analyze from a microeconomic standpoint the law’s impact on consumer behavior. In particular, a consumer behavioral analysis will model the impact of the law. It will assess the law’s impact on consumers and how consumers change their behavior accordingly.

The study shows how a law with a clear and precise purpose might generate unwanted (and potentially unexpected) drawbacks that go against the ratio legis, the rationale for enacting the law in the first place.

The Law

Indeed, the ratio legis of the 2022 reform is not to collect taxes but to reduce the costs associated with consuming junk food17. Unhealthy eating is seen as a negative externality, and taxation is seen as its remedy18. The logic goes as follows: by taxing those products (Pigouvian measure), their consumption decreases and thus the associated health costs19 will go down, as well. The tax discourages the consumption of taxed products while generating financial resources for backing up the care system20.

The law defines what qualifies a beverage as ultra-processed (and what is excluded) in art. 513 -1:

- liquid substance,

- with a maximum alcohol level of 0.5% vol.,

- to which sugar was added21

Art. 513-1 par. 1 Ley 2277 excludes medical treatments and baby formulas.

Art. 513-4 defines the tax (per 100ml). The tax shows a progression: the more sugar, the higher the amount of tax per 100ml22. The amount is found by multiplying the tax by volume (in ml) and dividing by 100.

Art. 513-6 defines what food is subject to taxation and art. 513-8/9 defines the amount (i.e., percentage of the sales price). All food to which sugars, salt, sodium and/or fats have been added (in an amount that is superior to a certain threshold) will be subject to this tax23.

Now, the tax is said to be hybrid, “hybrid, because it is specifically targeted at those ultra-processed foods that are high in fat, sugar, or salt”24. That is, according to this definition, two conditions must be met to fall under the tax: i) it should be an ultra-processed food, and ii) fat, sugar, and/or salt should reach a certain threshold. As a consequence, the Colombian tax overcomes the problem associated with putting a tax on all ultra-processed food, which is legally sensitive, by targeting the “nutrient profile of the product”, according to Sassi25. In other words, the Colombian law does not tax processed food per se, but only the processed food that exceeds certain legal parameters26, and thus is considered harmful. This strengthens the public health rationale of the measure27.

Economic analysis

After this presentation of the legal framework, we move on to analyze the junk food tax using economic theory. To this end, we will rely on microeconomics and address specific issues separately.

Junk food and Externalities

The law aims to solve a negative externality. An externality arises when someone’s action affects someone else28. A negative externality occurs when someone generates costs that are borne by others29. The generator of externality only accounts for the direct costs that he or she faces and not the indirect costs sustained by others30. The result is an overproduction of that good31. Externalities can fall on consumers or on producers32.

In the presence of negative externalities, the market fails to be efficient, and an intervention from the government is justified33. In that sense, the tax is economically justified. In particular, a possible solution is to tax those who generate externality to correct this inefficiency34. This tax is called a Pigouvian tax35. This is exactly the category under which Ley 2277 falls.

In casu, a producer of junk food does not sustain all the costs of consuming such food. The producer bears all the costs of manufacturing, packing, labeling and promoting the goods. The buyers consume the junk food. As seen above (supra), the consumer puts his health at risk. Statistically, those who consume those products eventually have to undergo medical treatments. The medical treatments come with extra costs. Those costs are sustained by the consumers (or the healthcare provider) and not by the producers. Thus, the producers do not account for those costs.

Two conclusions are to be reached. First of all, if the producers bear those costs, they will observe an increase in their marginal costs, and in fine reduce the quantity produced. In fact, the producer sells the quantity that maximizes their profit. From a microeconomics standpoint, this quantity is that one which ensures that their marginal costs are equal to the marginal revenue. By discarding the indirect cost related to the health cost, manufacturers account for a lower cost, and thus produce more than the optimal quantity (the one that covers all costs).

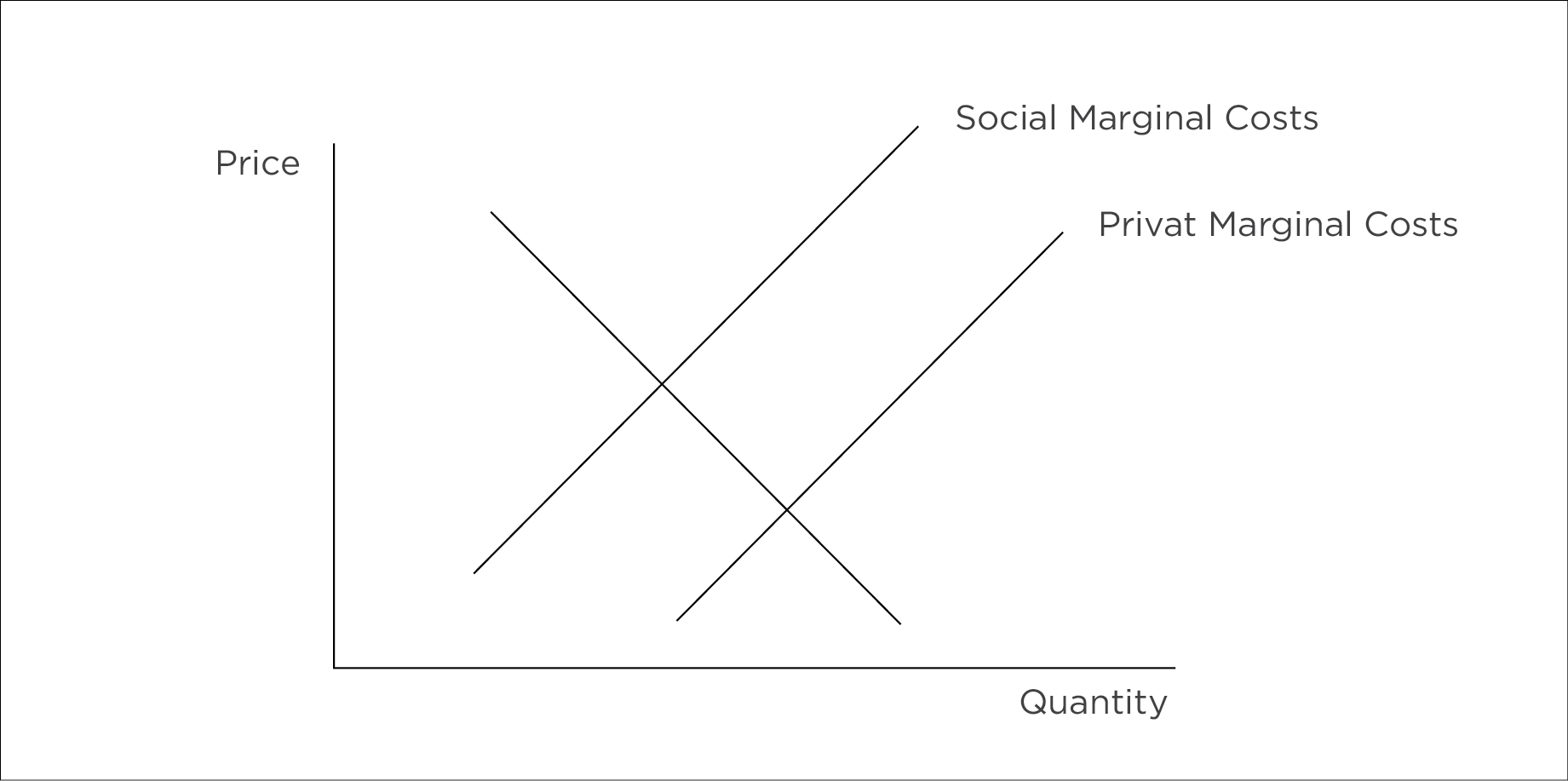

Figure 136 shows the situation graphically. The producer faces the private marginal cost of producing junk food, represented by the upward-sloping supply curve: as output increases, the marginal cost of production rises. However, the producer does not internalize the additional health costs imposed on society. When these external costs are added to the private marginal costs, we obtain the social marginal cost curve. Since the market equilibrium is determined by private costs alone, output exceeds the socially optimal level. This overproduction illustrates the classic case of a negative externality37.

The second conclusion is a corollary of the first. The price is lower, and the consumption of such goods is greater. The market produces a sub-optimal outcome, in which not all costs are correctly accounted for; there is overproduction of goods and overconsumption. The intervention of the Government is thus justified to correct the market failure.

Figure 1. Negative externalities

Source: Stiglitz, Economia del settore pubblico , 221.

Junk food and Elasticity

While the concept of externality tells us why a tax is needed, it does not tell us who would eventually pay for the tax. To analyze the direct effect of the tax, we should refer to the concept of elasticity. In particular, the price elasticity of demand and the supply determines how much of the tax is passed on to consumers and how much is incurred by producers.

The price elasticity of the demand is defined as the percentage change in the quantity demanded if the price increases by 1%38. Likewise, the price elasticity of supply is defined as the percentage change in the quantity supplied following an increase in price of 1%39.

Unless the demand is perfectly rigid, there is a drop in the quantity consumed40. The drop in consumed quantity increases with the demand’s elasticity (ceteris paribus). The elasticity also determines who bears the tax (financially).

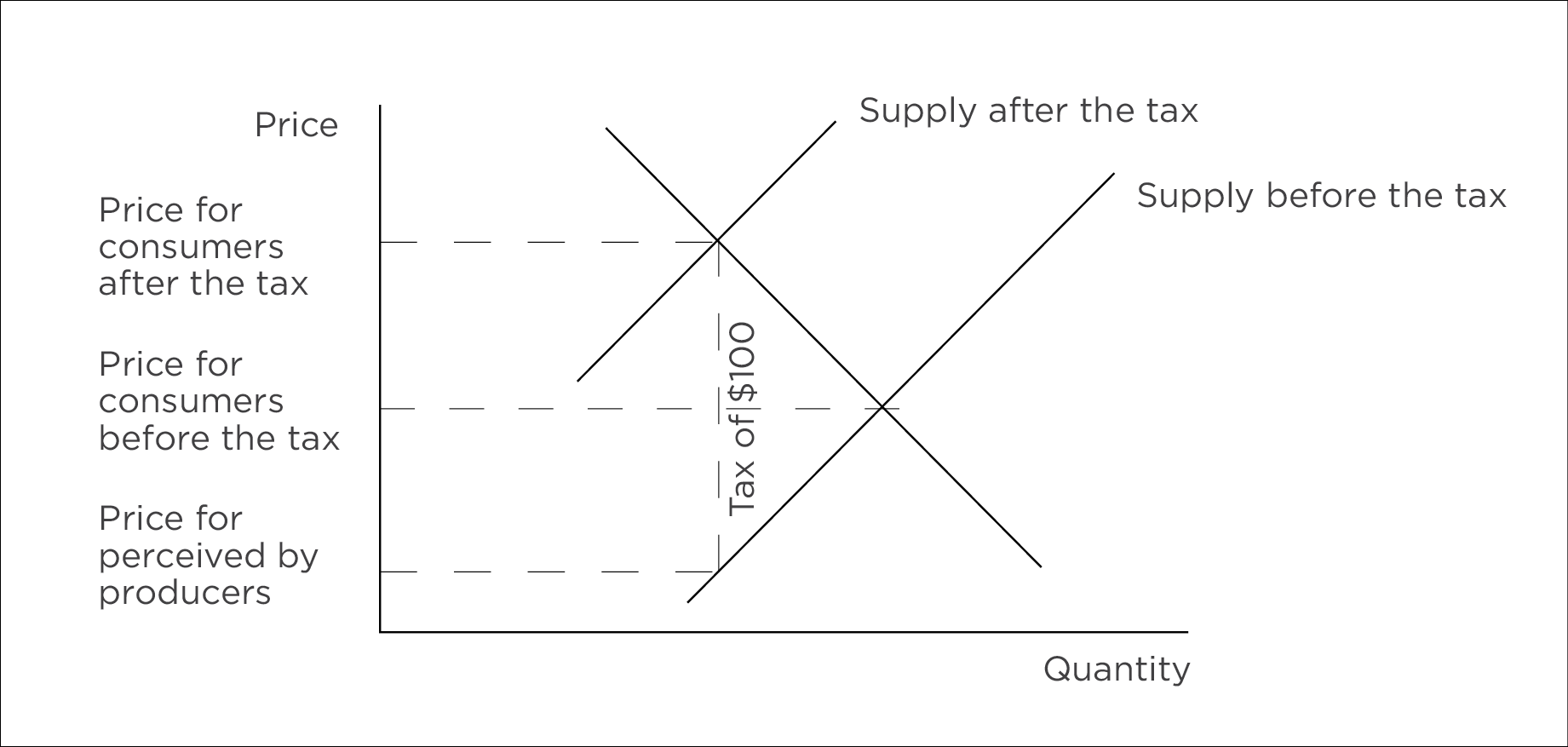

From an economic perspective, whether the tax is legally on the producer or the consumer does not determine who pays it41. To illustrate this, consider a perfectly competitive market42. Consider also a tax of $100 (per product sold) on the producer. Intuitively, we conclude that the producers will pay the tax. Nonetheless, the producer will try to pass the tax on to the consumer (increasing the price of the good). The more contractual power the producer has, the more it can increase the sales price. Let’s imagine that the manufacturer can only pass on $20 of the tax to the consumer. This would imply that it pays 80% of the tax and the consumer 20%. Figure 243 shows graphically the distribution of the $100 tax.

Figure 2. Effect of a tax on producers

Source: Stiglitz, Economia del settore pubblico, 292.

On the flip side, if a tax of $100 must be paid by consumers, then they will try to resist putting that product in their grocery cart. The producers will have to, if they want to keep selling their product, absorb part of the tax. The result will be the same: 80 for producers and 20 for consumers. All in all, it does not make a difference whether the policymaker labels it as a consumer or producer tax; the result is the same44.

For instance, we can consider the case in which consumers are insensitive to price changes (we say, in this case, that demand is considered ‘perfectly rigid’). If this is the case, the supplier can pass on 100% of the tax on the consumers45. In this case, the quantity of junk food consumed will remain unchanged, and consumers will just have to pay more for it, i.e. the entire amount of the tax. In efficiency terms, consumers are worse off. The extreme opposite scenario is a perfectly elastic demand46. In this case, the producers absorb the tax in full47, and the quantity demanded drops the most.

Generally, as the demand price elasticity decreases (or the price elasticity of supply increases), the tax shifts on to consumers’ shoulders48. On the contrary, as the price elasticity of demand increases, the effect on the quantity produced is more considerable.

This means that the effect of Ley 2277 on preventing health issues depends on the elasticity of the demand junk food in Colombia. If the demand for junk food is inelastic, the drop in quantity consumed is small, and the tax is mostly borne by its consumers. There would be only a modest redistribution of wealth from the taxpayer to those needing medical attention (assuming that the tax is actually used to sustain the health care system).

Generally, food and beverages tend to be inelastic49. However, the elasticity varies according to the type of product: the average demand price elasticity for fast food is -0.3050. In Chile, the elasticity for sweets and desserts is -0.812, for salty snacks it is -1.954, and for fats it is -0.93551.

This is in line with economic theory. Demand elasticity decreases (in absolute value) as the price decreases52. As junk foods tend to have low prices, a price increase or decrease does not affect consumers’ behavior massively. For instance, the demand for salt is not responsive to a change in price, as it is already low (and there are not many substitutes)53.

The price elasticity also differs according to the type of population. Firouz and Tsang find that unhealthy food and sodas are more elastic for educated people54. Thus, the authors concluded that, in the case of a junk food tax, people with a low education attainment level tend to bear a greater tax burden than educated consumers55. Also, the higher the elasticity, the lower the revenue (for the government) generated by the tax56.

From the above, we conclude that:

- Labeling a tax consumer or producer tax is meaningless as the effects are the same (supra);

- Junk food tends to be inelastic (in terms of demand price elasticity), meaning that the tax will mainly result in an increase in price (sustained by consumers) and a small reduction in consumption;

- People with lower education levels tend to bear these higher costs (supra);

- There is a trade-off: as elasticity increases, the tax is more effective in lowering consumption and the revenue generated is less (supra).

Substitution effect, Income effect, and Junk Food

After having established the rationale behind the tax (and its economic justification) and who pays for it, we turn our attention to the effect of the percentage of the tax that the consumer must pay for. Will this tax harm consumers’ budgets or will producers pay the most? The analysis below aims to study the “efficiency” of the tax, strictu sensu.

Formally, the (sub)session follows the Chicago School approach and analyzes the tax’s impact on consumers’ utility. When a tax is imposed on a good, two effects can arise: 1) The substitution effect (the consumer substitutes the taxed good for similar products) and 2) The income effect (consumers cut back on their overall consumption)57.

In theory, an increase in the price of junk food makes people healthier, which will translate into a drop in consumption of health services. On the other hand, the income effect of the tax means that consumers will have less to spend on healthcare and their income will drop58. Moreover, it is important to remember that all the tax revenue generated will, in an ideal world, be pumped into the healthcare system59. This compensation might induce consumers to start eating (at least some) junk food again.

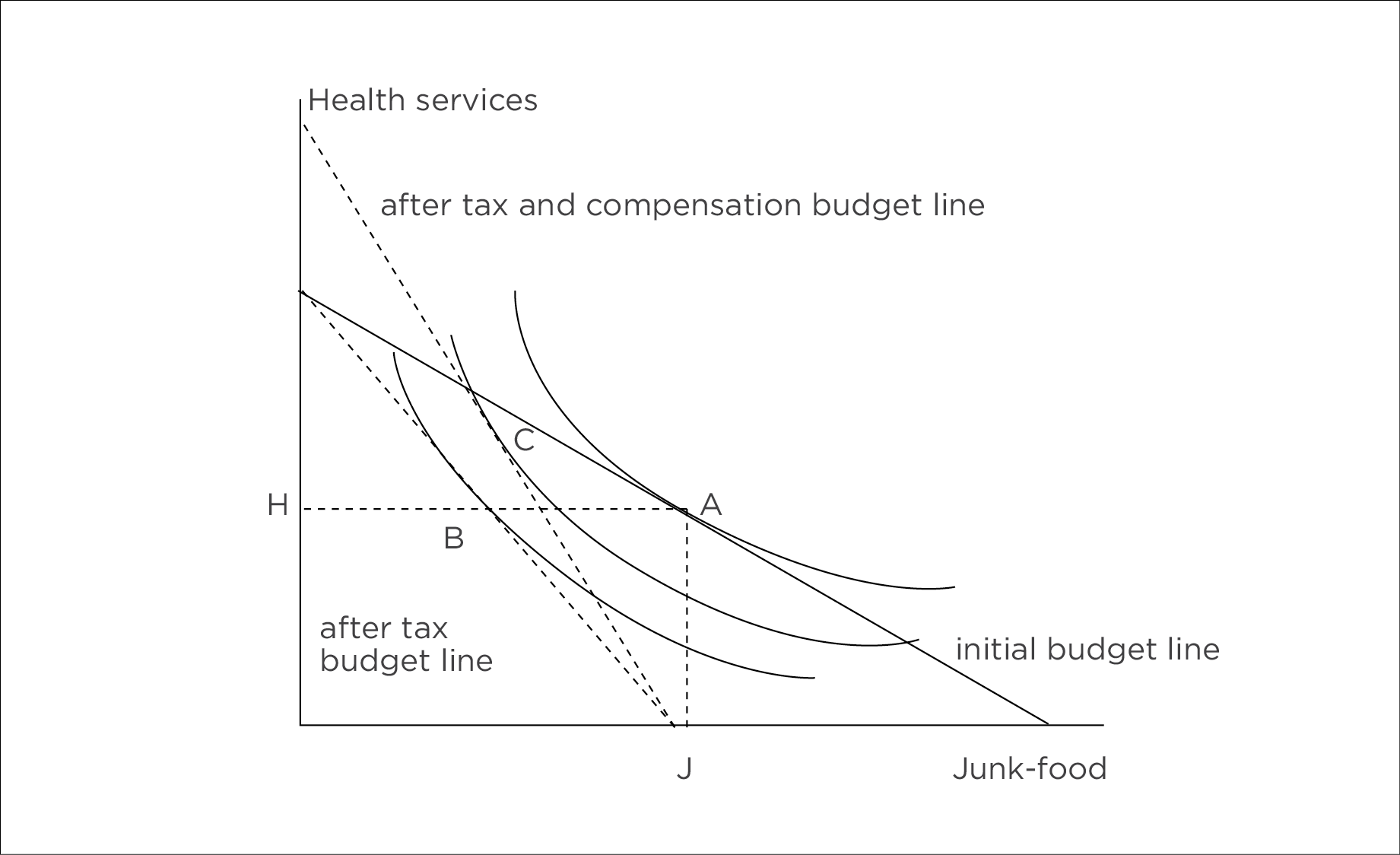

Let’s take a look at the traditional consumer-theory analysis (Figure 3) to see this point more clearly. Consider a consumer who must choose between two goods: junk food or health services (but the reasoning would also hold if we considered health services as income or, more technically, as the composite good). Given the initial budget line and the consumer’s indifferent curve, the consumer consumes bundle A (made of H units of health services and J units of junk food). Now, a tax on junk food would make the budget line steeper (in absolute value), depending on the elasticity of supply and demand (cf. supra). The consumer will rely on a lower indifference curve and consume fewer units of junk food (bundle B), while the effect on health services is unclear (cf. supra). Compensation for health services will further increase the budget line’s slope (in absolute value). The consumer will rely on a higher indifference curve and potentially consume more junk food (point C). Depending on the utility function, consumers can eventually consume more junk food as seen in point C (cf. Figure 4).

Figure 3. Consumer analysis.

Source: Figure by the author.

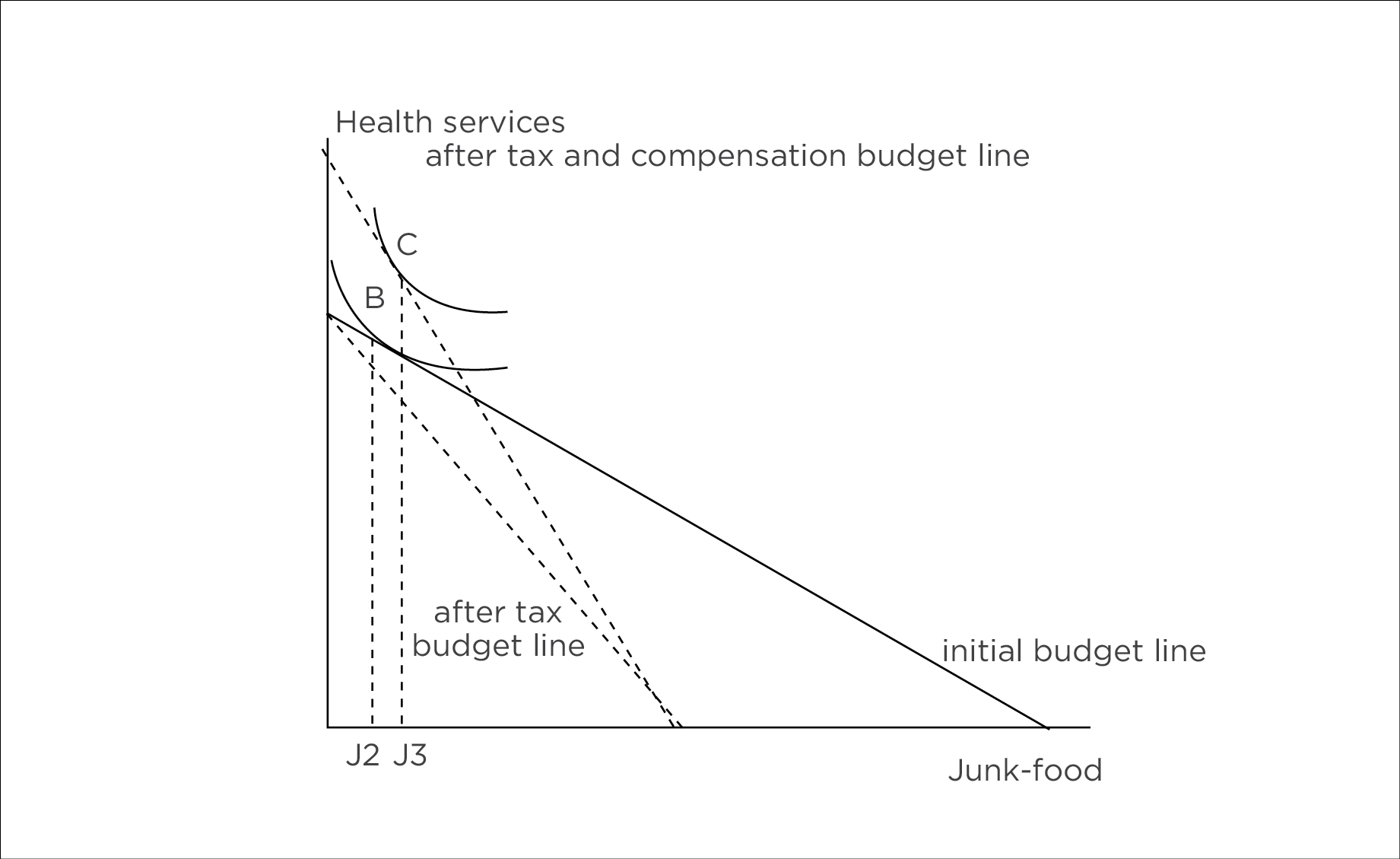

Figure 4 illustrates a situation where the overall effect increases junk food consumption. The situation depends on the marginal rate of substitution (MRS) of the two goods and the slope of the budget line (i.e., the relative price of the two goods) before and after the implementation of the tax and subsequent compensation.

Figure 4. Consumer analysis.

Source: Figure by the author.

The main takeaway here is that it is difficult to assess ex ante what the overall effect of a tax (and compensation) is ex post. The two components that determine the overall effect are the MRS and the price ratio between the two goods (junk food and health care services or, more generally, the composite good).

The MRS depends on the utility function. In other words, it depends on the preferences of the consumers. The MRS expresses the quantity of health services (or composite goods) a consumer should receive to compensate him or her for a loss in junk food. This ratio depends entirely on consumer preference, which is more the domain of psychology than economics. Thus, economic or legal variables cannot influence this first component. Indeed, a more informed choice can modify the MRS; but this cannot be ascertained through a legal or economic approach.

In this context, the only thing the policymaker can do is to influence the price ratio. Without knowing the MRS, however, it can only proceed empirically. In other words, the policymaker can set a tax, see what happens, adjust it, and re-lap (in a reiterative process) until it reaches the desired effect. There is no guarantee of success here as it is not possible to rule out extreme solutions (such as corner solutions or perfectly complementary goods). Assuming a “desired” solution exists, the policymaker should collect data, analyze it and subsequently adjust the law.

Conclusion

This study conducted an economic analysis of the recently introduced Ley 2277 in Colombia. The law aims to curb junk food consumption, which is associated with an increase in diabetes, obesity and menstruation problems60, let alone mental health, anxiety, and depression issues61.

In economic terms, junk food constitutes a negative externality: producers sustain the cost of producing and selling it but not the cost generated by its consumption. This results in the private cost being lower than the social cost. Economic theory justifies governmental intervention. Among the solutions available to the government, one is to tax the consumption of such a good. The Colombian government decided to levy a tax on junk food manufacturers (and use the revenue generated to bolster the finances of the health sector).

The economic analysis demonstrates that governmental intervention is justified, as the market fails to produce the most efficient outcome (supra). Moreover, it shows that the statutory incidence of the tax —whether formally imposed on producers or consumers— is irrelevant. In equilibrium, both sides share the burden, and the distribution depends on the relative elasticities of supply and demand for junk food. Specifically, the less elastic (more rigid) the demand, the greater the share of the tax borne by consumers; conversely, the less elastic the supply, the greater the share borne by producers.

The empirical analysis shows that, in general, junk food tends to be inelastic (supra). Thus, a tax on it will only partially reach its goal as it might only modestly reduce its consumption. Moreover, applied economics shows that people with lower education attainment levels tend to have a less elastic demand (compared to more educated individuals). Consequently, uneducated consumers are likely to bear the brunt of the tax (supra) and only slightly curb their junk food consumption (supra).

Finally, consumer behavior analysis indicates that using tax revenues to fund the health sector might undermine the desired effect (and work against the ratio legis). In fact, the compensation received might paradoxically induce people to consume more junk food. Intuitively, consumers who pay more for junk food but less for healthcare will have more money in their pockets and will, therefore, be more inclined to buy greater quantities of unhealthy foods and beverages.

The evidence on reduced consumption is particularly relevant for low-income households. However, these households often face fewer and more costly alternatives to ultra-processed food, especially given the recent inflationary pressures on healthier products62. This situation exacerbates their vulnerability, as they must either absorb the tax burden or allocate a larger share of their income to substitute goods. In turn, the unequal access to affordable, healthy options reinforces the need for complementary policies. Moreover, low-income consumers are more likely to depend on the social security system to cover the health costs associated with diet-related diseases, in contrast to higher-income groups who can afford private healthcare. These considerations highlight the distributive dimension of the tax and the importance of integrating it with broader social policies.

All in all, this article represents an economic analysis of the Colombian junk food tax. It shows how using a “simple” tax with a clear (and worthwhile) purpose—namely, to correct consumers’ behavior—has complex implications that may contradict the ratio legis. The tax’s ultimate purpose is to improve the lives of junk food consumers by inducing them to adopt healthier diets and thereby reducing disease incidence. However, in practice, the measure has also functioned as a revenue-raising device. Given the absence of conclusive evidence of significant changes in eating habits or reductions in diet-related pathologies, this dual role may be interpreted as diverging from the original legislative intent.

At the same time, recent preliminary evidence suggests that the tax may already be beginning to affect consumer behavior. A 2024 market report indicates an apparent reduction of around 5% in the consumption of ultra-processed foods compared to pre-tax levels (FoodNavigator, 2024). While this evidence is not yet academic and should be interpreted cautiously, it provides early signals that the measure could have the intended effect of discouraging unhealthy consumption.

The microeconomic analysis further suggests that the tax might result in a heavier burden for consumers without significantly modifying their habits. It also indicates that the incidence may fall disproportionately on less educated consumers, while more educated and affluent groups can more easily avoid taxed products. Finally, it highlights how a restitution policy might operate as a boomerang effect, limiting the potential positive outcomes of the measure.

In conclusion, the economic analysis might reveal how a lex might miss its target and generate unexpected drawbacks.

This study does not aim to be a conclusive work but a starting point for a broader discussion. This study has two main limitations. Firstly, it was not possible to conduct an econometric analysis of the effect of taxation on consumers’ behavior. This limitation is due to the lack of data. Figures on Colombian junk food consumption are limited by the fact that the law was implemented very recently. Consumers need time to adjust their behavior, and it will take time to see if better healthcare outcomes are achieved in Colombia. Indeed, health is a lagging indicator, which brings us to limitation number two. Economic analysis needs to be combined with an epidemiological analysis. In fact, while economic theory might indicate that the impact on consumer behavior is limited, it cannot determine if the impact is meaningful or not. Does a drop of 0.1%, 1%, or 10% in junk food consumption alter the course of the country’s overall health outcomes? Is it enough to extend the lifespan of Colombians or increase their quality of life? This question needs epidemiological and medical studies address it. After all, the question of whether Colombians are healthier in the long run is undoubtedly more important than considerations pertaining to economic theory.

Additionally, civil society commentary adds nuanced perspectives on the Colombian tax policy, and consensus remains far from being reached. Dejusticia, a leading Colombian think tank on law and social justice, describes the measure as a cautious yet imperfect advance, emphasizing how relatively low tax thresholds and industry lobbying have limited its potential health impact63. From an international standpoint, the PAHO/WHO underscores the broader policy rationale behind “[i]mpuestos saludables” framing them as multipurpose tools that simultaneously discourage the consumption of harmful products, prevent noncommunicable diseases, generate sustainable fiscal revenues, and reduce health inequities64. Finally, national press coverage illustrates how the debate continues to evolve in the public sphere; for instance, El Tiempo has highlighted concerns over the influence of the beverage and ultra-processed food industry in shaping both the tax and related food-labeling regulations65.

Acknowledgement

The author wants to thank Ms. Eliana Katherine Vega Rojas, attorney at law, for her insights.

Bibliography

- Andreyeva, Tatiana, Michael W. Long, and Kelly D. Brownell. «The Impact of Food Prices on Consumption: A Systematic Review of Research on the Price Elasticity of Demand for Food». American Journal of Public Health 100, n.o 2 (2010): 216-22. https://doi.org/10.2105/AJPH.2008.151415.

- Angarita, Ghina, and Erika Reina. “Expectativa en la implementación de los impuestos saludables en Colombia, desde la experiencia de Chile y México”. Universidad libre. 2023. https://repository.unilibre.edu.co/bitstream/handle/10901/27637/Final%20-%20GT%20-%20Angarita%20y%20Reina.pdf?sequence=1&isAllowed=y.

- BéndiksenLaw. «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS». BéndiksenLaw, December 31, 2023. https://www.bendiksenlaw.co/icui-law-2277-of-2022-and-dian-rulings/.

- Burki, Talha. «New Junk Food Legislation in Colombia». The Lancet Oncology 24, n.o 12 (2023). https://doi.org/10.1016/S1470-2045(23)00591-0.

- Caro, Juan Carlos, Shu Wen Ng, Lindsey Smith Taillie, and Barry M. Popkin. «Designing a tax to discourage unhealthy food and beverage purchases: The case of Chile». Food Policy 71 (2017): 86-100. https://doi.org/10.1016/j.foodpol.2017.08.001.

- Congreso de la República de Colombia, Ley 2277 de 2022, “Por medio de la cual se adopta una reforma tributaria para la igualdad y la justica social y se dictan otras disposiciones”, Diario Oficial No. 52.247, December 13, 2022.

- Dejusticia. «Colombia por fin tendrá un impuesto saludable: ¿por qué es un avance imperfecto?» Dejusticia, November 24, 2022. https://www.dejusticia.org/colombia-por-fin-tendra-un-impuesto-saludable-por-que-es-un-avance-imperfecto/.

- Ejtahed, Hanieh-Sadat, Parham Mardi, Bahram Hejrani, et al. «Association between junk food consumption and mental health problems in adults: a systematic review and meta-analysis». BMC Psychiatry 24, n.o 1 (2024): 438. https://doi.org/10.1186/s12888-024-05889-8.

- Eldridge, Stephen. 2023. “Negative Externality.” Encyclopedia Britannica, July 7, 2023. https://www.britannica.com/topic/negative-externality.

- El Tiempo. «Minsalud se pronuncia sobre ley de etiquetado de comida chatarra». November 17, 2021. https://www.eltiempo.com/salud/minsalud-se-pronuncia-sobre-ley-de-etiquetado-de-comida-chatarra-667660.

- Firouz, Gahvari, and Harry Tsang. “Optimal Taxation and Junk Food”. Working paper, 2013.

- Frank, Robert. Microeconomics and Behavior. 10.a ed. McGraw-Hill/Irwin, 2024.

- Gómez, Eduardo J. «Getting to the root of the problem: the international and domestic politics of junk food industry regulation in Latin America». Health Policy and Planning 36, n.o 10 (2021): 1521-33. https://doi.org/10.1093/heapol/czab100.

- Listokin, Yair. «Law and Macroeconomics: The Law and Economics of Recessions». Yale Journal on Regulation 34, n.° 3 (2017): 791–854.

- Lozano Rodríguez, Eleonora, and Francisco Soler-Peña. «Una aproximación al análisis macroeconómico del derecho: La tributación y las condiciones de existencia del mercado». In Estudios interdisciplinarios de la tributación, ed. Eleonora Lozano Rodríguez. Universidad de los Andes, 2022.

- Lucas, Robert E. «Econometric Policy Evaluation: A Critique». Carnegie-Rochester Conference Series on Public Policy 1, n.° 1 (1976): 19–46.

- Meyer, Katie A., David K. Guilkey, Shu Wen Ng, et al. «Sociodemographic Differences in Fast Food Price Sensitivity». JAMA Internal Medicine 174, n.o 3 (2014): 434-42. https://doi.org/10.1001/jamainternmed.2013.13922.

- Northwell Health. “How Inflation Is Hurting the Diets of Low-Income Americans.” February 13, 2025. https://www.northwell.edu/news/the-latest/inflation-and-american-diets.

- Pan American Health Organization. Health Taxes. Washington, DC: PAHO/WHO. Accessed August 23, 2025. https://www.paho.org/es/temas/impuestos-saludables.

- Real, Camila. Colombia Declares War on Junk Food | Inter-American Law Review. November 21, 2023. https://inter-american-law-review.law.miami.edu/colombia-declares-war-on-junk-food/.

- Shinde, Prashant, Kavita Vyas, Sumeet Goel, and Om Raj Sharma. «Effects of Junk Food/Fast Food on Menstrual Health: A Review Study». International Ayurvedic Medical Journal 2, n.° 1 (2017): 866-871. http://www.iamj.in/posts/images/upload/866_871.pdf.

- Soler-Peña, Francisco. Análisis macroeconómico del derecho. Master’s and doctoral thesis. Bogotá: Universidad de los Andes, 2021.

- Stiglitz, Joseph E. Economia del settore pubblico – Volume primo – Fondamenti Teorici. 2nd ed. Milan: Hoepli, 2003.

- Strzyżyńska, Weronika. «Colombia Passes Ambitious ‘Junk Food Law’ to Tackle Lifestyle Diseases». Global Development. The Guardian, November 10 2023. https://www.theguardian.com/global-development/2023/nov/10/colombia-junk-food-tax-improve-health-acc.

- Swinburn, Boyd A. «Obesity prevention: the role of policies, laws and regulations». Australia and New Zealand Health Policy 5, n.o 1 (2008). https://doi.org/10.1186/1743-8462-5-12.

- Taylor, Luke. «Colombia Introduces Latin America’s First Junk Food Tax». News. BMJ 383 (2023): 2698. https://doi.org/10.1136/bmj.p2698.

- Varian, Hal R. Microeconomic Analysis. 3rd ed. New York: W. W. Norton & Company, 1992.

- Woodford, Michael. Interest and Prices: Foundations of a Theory of Monetary Policy. Princeton, NJ: Princeton University Press, 2003.

___________________________________________________________________________

* Dr. Giuliano Bianchi is an economist and jurist, and Associate Professor of Economics at EHL. He is Co-Director of the Quantitas Institute and conducts research on law and economics, corporate governance, and forecasting. Previously, he was a Wertheim Fellow at Harvard Law School, focusing on corporate governance. His work has been published in international refereed journals and industry reports. Dr. Bianchi holds a PhD in Economics from the University of Bologna, a BA in Economics from Lugano, an MSc in Economics from Edinburgh, a BLaw from UniDistance, and an MLaw from Fribourg. ORCID: https://orcid.org/0000-0002-5766-6933.

1 A broader economic analysis could also adopt a macroeconomic perspective, as discussed by Lozano and Soler-Peña (2021), Soler-Peña (2021), and Listokin (2017), or an econometric one. We note, however, that under the current mainstream neoclassical synthesis, macroeconomic theory is generally micro-founded (Lucas, 1976; Woodford, 2003). Since microeconomics is a subsection of economics, we use the two terms microeconomic analysis and economic analysis interchangeably in this article.

2 Luke Taylor, «Colombia Introduces Latin America’s First Junk Food Tax», News, BMJ 383 (noviembre de 2023): p2698, https://doi.org/10.1136/bmj.p2698.

3 Weronika Strzyżyńska, «Colombia Passes Ambitious ‘Junk Food Law’ to Tackle Lifestyle Diseases», Global Development, The Guardian, 10 de noviembre de 2023, https://www.theguardian.com/global-development/2023/nov/10/colombia-junk-food-tax-improve-health-acc.

4 (Shinde et al. 2017)

5 Hanieh-Sadat Ejtahed et al., «Association between junk food consumption and mental health problems in adults: a systematic review and meta-analysis», BMC Psychiatry 24, n.o 1 (2024): 438, https://doi.org/10.1186/s12888-024-05889-8.

6 Camila Real, Colombia Declares War on Junk Food, November 20, 2023, https://inter-american-law-review.law.miami.edu/colombia-declares-war-on-junk-food/.

7 Real, Colombia Declares War on Junk Food.

8 Boyd A. Swinburn, «Obesity prevention: the role of policies, laws and regulations», Australia and New Zealand Health Policy 5, n.o 1 (2008): 12, https://doi.org/10.1186/1743-8462-5-12.

9 Eduardo J Gómez, «Getting to the root of the problem: the international and domestic politics of junk food industry regulation in Latin America», Health Policy and Planning 36, n.o 10 (2021): 1521-33, https://doi.org/10.1093/heapol/czab100; Swinburn, «Obesity prevention».

10 Ghina Angarita, and Erika Reina. “Expectativa en la implementación de los impuestos saludables en Colombia, desde la experiencia de Chile y México”. Universidad libre (2023).

11 Talha Burki, «New Junk Food Legislation in Colombia», The Lancet Oncology 24, n.o 12 (2023), https://doi.org/10.1016/S1470-2045(23)00591-0.

12 Angarita and Reina, “Expectativa en la implementación de los impuestos saludables”.

13 Angarita and Reina, “Expectativa en la implementación de los impuestos saludables”.

14 Burki, «New Junk Food Legislation in Colombia».

15 Burki, «New Junk Food Legislation in Colombia».

16 Joseph Stiglitz, Economia del settore pubblico – Volume primo – Fondamenti Teorici, (Milan: Hoepli, 2003): 56.

17 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS», BéndiksenLaw, 31 de diciembre de 2023, https://www.bendiksenlaw.co/icui-law-2277-of-2022-and-dian-rulings/.

18 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS».

19 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS».

20 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS».

21 Congreso de la República de Colombia, Ley 2277 de 2022, “Por medio de la cual se adopta una reforma tributaria para la igualdad y la justica social y se dictan otras disposiciones”, Diario Oficial No. 52.247, December 13, 2022.

22 Congreso de la República de Colombia, Ley 2277 de 2022, “Por medio de la cual se adopta una reforma tributaria para la igualdad y la justica social y se dictan otras disposiciones”, December 13, 2022.

23 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS».

24 Burki, «New Junk Food Legislation in Colombia».

25 As cited on Burki, «New Junk Food Legislation in Colombia».

26 Burki, «New Junk Food Legislation in Colombia».

27 Burki, «New Junk Food Legislation in Colombia».

28 Hal R. Varian, Microeconomic Analysis, (New York: W. W. Norton & Company, 1992): 432.

29 (Eldridge 2023)

30 Varian, Microeconomic Analysis, 433.

31 Varian, Microeconomic Analysis, 433.

32 Varian, Microeconomic Analysis, 432.

33 Stiglitz, Economia del settore pubblico, 56.

34 Varian, Microeconomic Analysis, 433.

35 Varian, Microeconomic Analysis, 433.

36 The figure is an adaptation of Figure 8.1. in Stiglitz, Economia del settore pubblico, 221.

37 cf. Stiglitz, Economia del settore pubblico, 221.

38 Stiglitz, Economia del settore pubblico, 299.

39 Stiglitz, Economia del settore pubblico, 300.

40 cf. Stiglitz, Economia del settore pubblico, 292.

41 Stiglitz, Economia del settore pubblico, 292.

42 The analysis of a competitive market is inspired by Stiglitz, Economia del settore pubblico, 290.

43 Figure 2 is a readaptation of Figure 10.2 in Stiglitz, Economia del settore pubblico,292.

44 Stiglitz, Economia del settore pubblico, 295.

45 For a technical exposition, cf. Stiglitz, Economia del settore pubblico, 297.

46 For a technical exposition, cf. Stiglitz, Economia del settore pubblico, 297.

47 Stiglitz, Economia del settore pubblico, 298.

48 Stiglitz, Economia del settore pubblico, 299.

49 Tatiana Andreyeva et al., «The Impact of Food Prices on Consumption: A Systematic Review of Research on the Price Elasticity of Demand for Food», American Journal of Public Health 100, n.o 2 (2010): 218, https://doi.org/10.2105/AJPH.2008.151415.

50 Katie A. Meyer et al., «Sociodemographic Differences in Fast Food Price Sensitivity», JAMA Internal Medicine 174, n.o 3 (2014): 434-42, https://doi.org/10.1001/jamainternmed.2013.13922.

51 Juan Carlos Caro et al., «Designing a tax to discourage unhealthy food and beverage purchases: The case of Chile», Food Policy 71 (2017): 86-100, https://doi.org/10.1016/j.foodpol.2017.08.001.

52 Robert Frank, Microeconomics and Behavior, 10.a ed. (McGraw-Hill/Irwin, 2024).

53 Frank, Microeconomics and Behavior.

54 Gahvari Firouz, and Harry Tsang, «Optimal Taxation and Junk Food», Working paper, (2013): 16.

55 Firouz and Tsang, «Optimal Taxation and Junk Food», 16.

56 Firouz and Tsang, «Optimal Taxation and Junk Food», 16.

57 Stiglitz, Economia del settore pubblico, 335.

58 Cf. Frank, Microeconomics and Behavior.

59 BéndiksenLaw, «Colombia - Junk Food Tax - LAW 2227 OF 2022 AND DIAN RULINGS».

60 Prashant Shinde, «Effects of Junk Food/Fast Food on Menstrual Health: A Review Study». International Ayurvedic Medical Journal 2, n.° 1 (2017): 866-871.

61 Ejtahed et al., «Association between junk food consumption and mental health problems in adults».

62 Recent reporting shows that inflation is disproportionately raising the prices of healthier food options, making them less affordable for low-income households (Northwell Health, 2025).

63 Dejusticia, «Colombia por fin tendrá un impuesto saludable: ¿por qué es un avance imperfecto?», Dejusticia, 24 de noviembre de 2022, https://www.dejusticia.org/colombia-por-fin-tendra-un-impuesto-saludable-por-que-es-un-avance-imperfecto/.

64 Pan American Health Organization. Health Taxes. Washington, DC: PAHO/WHO. Accessed August 23, 2025. https://www.paho.org/es/temas/impuestos-saludables.

65 El Tiempo. «Minsalud se pronuncia sobre ley de etiquetado de comida chatarra». November 17, 2021. https://www.eltiempo.com/salud/minsalud-se-pronuncia-sobre-ley-de-etiquetado-de-comida-chatarra-667660.